Bondshala

Expert Tips, News, Views & Everything You Want To Know

Expert Tips, News, Views & Everything You Want To Know

Know why you should not be irritated by KYC compliance; they protect your money

FOMO and upgrade mania will make wealth generation skid

NDTV Profit - Full Interview Suresh Darak on Debt Market

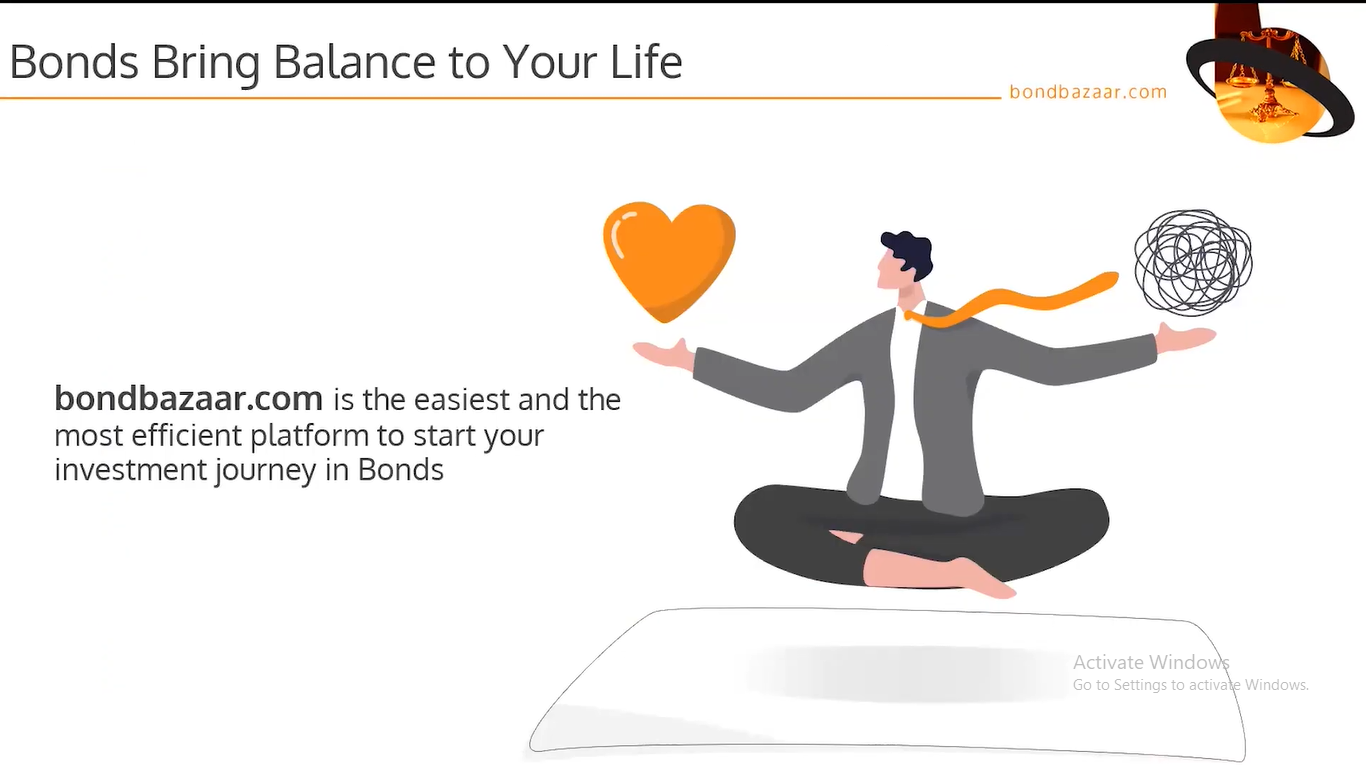

Bonds Bring Balance To Your Portfolio English

Bonds Bring Balance To Your Portfolio Hindi

Bond Price Calculation English

Bond Price Calculation (Hindi)

Trading in the Secondary Market (English)

Trading in the Secondary Market (Hindi)

Selecting A Bond (English)

Webinar for Customers - Detailed session on Sovereign Gold Bonds

Webinar for Customers - Taxation of Bonds